By Wesley Fricks

The previous article in this series introduced HB 1042 and the Blue Ridge property tax exemption it would narrow. The bill, which passed the NC House on Thursday and is on its way to the NC Senate, is driven primarily by revenue concerns as municipalities are highlighting the lost tax revenue because of the exemption.

Wake County’s concern, probably the loudest voice in recent legislative hearings, is the roughly $11.4 million in foregone county tax revenue in 2025 from properties using the exemption. Lost revenue is certainly one definition of cost.

A different lens could consider the actual cost compared to other delivery methods: how much does it cost to preserve a below-market unit, and how much does it take to build a new one? Let’s look at two recent data points and run the math. The answer matters as the legislature decides what to do with the exemption and determines if both approaches can live under the same roof.

What the Exemption Costs

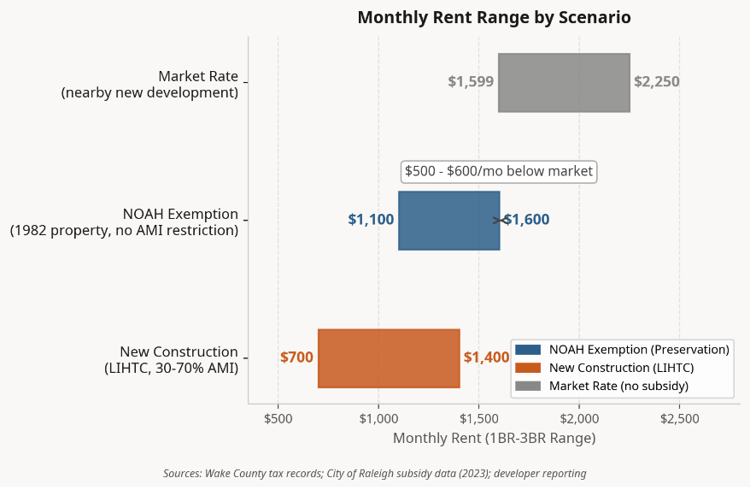

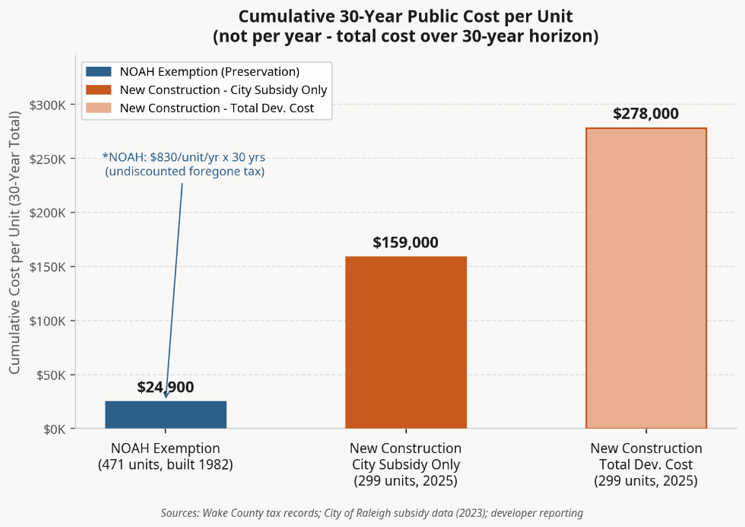

Take a 471-unit property in north Raleigh operating under the exemption. Its 2024 tax bill, before exemption in 2025, was $391,478. That is roughly $830 per unit per year in foregone tax revenue to Wake County and the City of Raleigh combined.

The property was built in 1982. Its advertised rents range from $1,100 for a one-bedroom up to $1,600 for a three-bedroom unit. A newer development nearby opened recently and advertises one-bedrooms from $1,599 up to $2,250 for three-bedrooms.

The exempted property is $500 to $600 per month below the newer property across unit types. Instead of the owner executing a business plan to close the rent gap, the property tax exemption provides incentive to keep rents in the current range, thereby preserving naturally occurring below-market housing.

What New Construction Costs

Two new income-restricted communities in Raleigh opened earlier this month. Birch & Branch in North Raleigh delivered 180 units at 30 to 70 percent AMI. The Pines at Peach in South Raleigh delivered 119 units at 30 to 60 percent AMI.

Combined project cost was reportedly more than $83 million across 299 units, or roughly $278,000 per unit. The capital stack required to deliver them included federal housing tax credits from the North Carolina Housing Finance Agency, tax-exempt bonds from the Raleigh Housing Authority, gap financing from both the City of Raleigh and Wake County, a city ground lease on one site, and a road extension built to support the other. Private equity from the developer covered the balance.

The City of Raleigh’s own subsidy data, as of 2023, reports that the average public subsidy required to create one new rental unit restricted at 60 percent AMI is $159,000. That figure is the direct city contribution and does not include the federal tax credit equity, bond financing, or the foregone property tax revenue going forward. Income-restricted housing typically continues to qualify for property tax exemption throughout its covenant period, often 30 years or longer.

All of the Above Approach

The two tools serve different parts of the housing market. New construction at 30 to 70 percent AMI adds deeper-targeted units that did not exist before. The Blue Ridge exemption at 80 percent AMI applies to existing properties with rents already below that ceiling.

Note: Preserved and newly built units serve different AMI bands and populations; the comparison is of public cost per unit, not of identical products.

On a dollars-per-unit basis, producing a new income-restricted unit in this example runs roughly $278,000 in total development costs, layered across federal credits, local bonds, city and county subsidies, and private equity. Of that, the city subsidy alone is about $159,000 per unit. And that figure still doesn’t count the time to deliver or the ongoing property tax exemption.

The cost of keeping an existing below-market unit in service through the exemption is $830 per unit per year and can be implemented immediately since the units already exist.

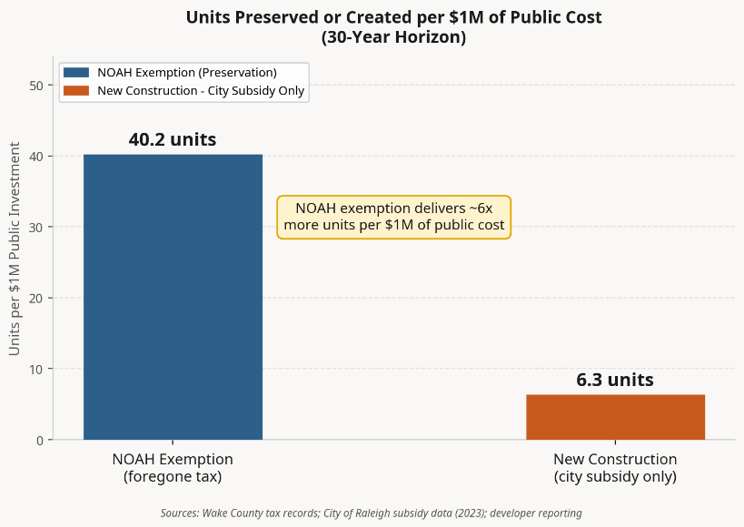

The math is pretty clear: the exemption preserves roughly 40 units per $1 million of public cost, but that $1 million is spread over 30 years at $830 per unit per year, with no upfront capital commitment. New construction, by contrast, requires about $159,000 in city subsidy per unit at closing before a single tenant is housed, and that’s only the local slice of a $278,000 total. The ongoing property tax exemption then adds to the cost for decades after.

What This Means for Wake County and Beyond

This math in Wake County points toward an all-of-the-above approach. New construction delivers units at deeper AMI bands that do not exist today, but at a per-unit cost that limits how far public subsidy can scale. The existing exemption retains units that are already priced below market at a fraction of that cost, but only functions if the framework survives legislative review.

Preserving existing below-market housing and incentivizing new supply are not competing strategies. They operate at different price points, serve different populations, and rely on different capital structures. Losing either tool narrows the options in a market that is running out of them.

HB 1042 will be debated on its revenue merits in committee. The cost math is a separate but parallel question that the legislature should engage with. If the bill narrows the exemption so far that meaningful numbers of currently below-market units lose their preservation incentive, replacing those units through new construction is several orders of magnitude more expensive per unit. That cost falls on city and county budgets, state and federal tax credits, and the patience of developers willing to coordinate four or five layers of financing. None of those resources are unlimited.

For owners and operators in North Carolina, this policy change would influence underwriting if it passes. The uncertainty around it now adds a new layer of ice to an already frigid multifamily landscape. Markets need clarity.

If you have a property currently using the exemption, or you are underwriting an acquisition where exempted comps influence pricing, this is the time to model both sides.

Contact

Wesley Fricks

wfricks@greysteel.com

919.746.9909

More Real Estate Insights

THOUGHT LEADERS

Why Capital Is Moving into the Midwest Multifamily Market and Why It’s Here to Stay

THOUGHT LEADERS

NC Property Tax Reform, Part 3: Preserve or Build? The Cost Math on Workforce Housing Wake County, NC, in Focus

THOUGHT LEADERS

Rent Growth in Midwest Multifamily Markets: Why Consistency Is Outperforming Volatility

Greysteel Advisory Expertise

Greysteel is a commercial real estate advisory firm specializing in investment sales and debt and structured finance, serving institutional clients, private investors, and middle-market operators nationwide.

The firm provides sector-focused advisory across all asset classes, delivering market intelligence, capital markets expertise, and disciplined execution.