By Wesley Fricks

Takeaways from the Greysteel Carolinas Multifamily Event in Raleigh, North Carolina, featuring rental housing economist Jay Parsons and NC Commerce’s Kenny Flowers

For much of the past decade, multifamily investing in the Carolinas followed a predictable formula: target high-growth markets, rely on population inflows, and let rent growth drive returns. That formula worked. It is no longer sufficient.

At the Greysteel Carolinas Multifamily Event in April, economist Jay Parsons and North Carolina Chief Deputy Secretary of Commerce Kenny Flowers laid out the case that the region is not losing momentum. It is evolving. The Carolinas are moving into an environment where outcomes depend less on broad market growth and more on supply timing, submarket selection, and execution.

The Problem Is Supply, Not Demand

The current softness in Carolinas apartment markets is not a demand story. In 2025, the Carolinas absorbed 9% of all U.S. apartment demand, well above the region’s share of national inventory. Net absorption remains above the long-term average both locally and nationally.

What changed is supply. U.S. apartment completions hit roughly 590,000 units in 2024, a level not seen in decades. Charlotte, Raleigh, Charleston, and Greenville all experienced significant inventory expansion. In several submarkets, that new supply temporarily outpaced absorption, pushing up vacancy, elevating concessions, and compressing rents.

That wave is now breaking. National completions are projected to fall to approximately 312,000 units in 2026 and continue declining. Construction starts have reset to 2013-2014 levels. Across the Carolinas, supply expansion rates are dropping sharply from their cycle peaks. The pipeline is clearing.

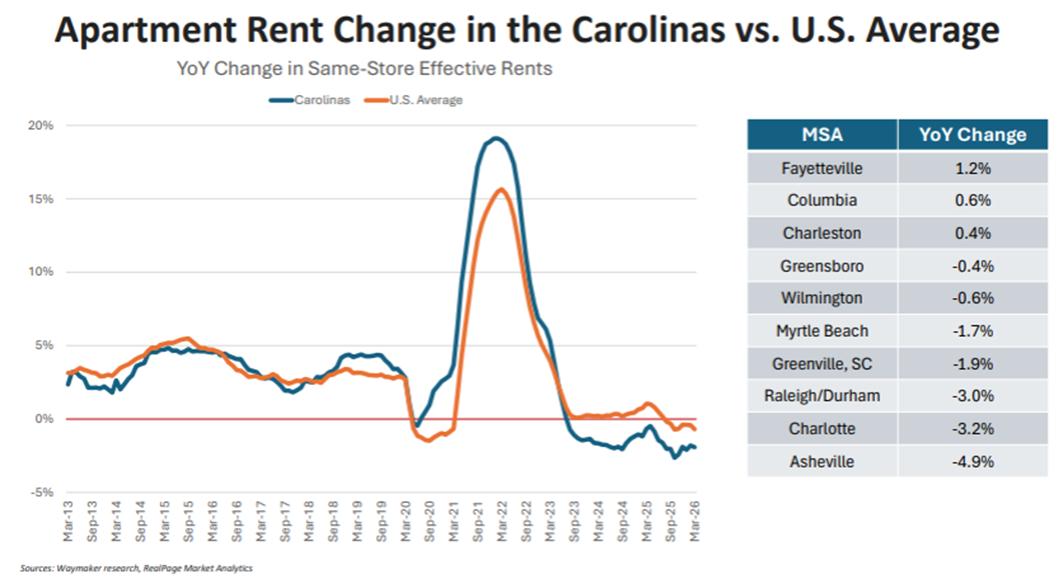

Rent Recovery Is Underway, But Uneven

Charlotte (-3.2% year-over-year effective rent change) and Raleigh/Durham (-3.0%) remain under pressure. Concession values are elevated: 12.7% in Charlotte, 11.6% in Raleigh. These are the markets that absorbed the most new supply, and they are working through it.

Meanwhile, less-supplied metros have already turned. Fayetteville is posting +1.2% rent growth, Columbia +0.6%, Charleston +0.4%. Most Carolinas metros are showing improvement relative to their trailing-12-month lows, even where year-over-year numbers are still negative. The direction has shifted; the magnitude has not caught up.

The affordability picture supports continued recovery. Wage growth has outpaced rent growth for 38 consecutive months nationally. In Q1 2026, median rent-to-income ratios for new lease signers stand at 21.4% in Raleigh/Durham and 22.5% in Charlotte. Renters can absorb rent increases when they come. The constraint has been supply, not purchasing power.

Don’t Benchmark Against 2021

A recurring theme in the discussion was the tendency to measure today’s performance against the extraordinary results of 2021 and 2022. By that standard, the current market looks weak. By any other standard, it looks like a market returning to normal.

Rent growth has moderated. Household formation continues. The structural drivers behind Carolinas demand, including job creation, population growth, and economic diversification, have not reversed. They have normalized. Investors who interpret this normalization as deterioration will misprice both the risk and the opportunity.

Capital Is Back, But the National Playbook Doesn’t Apply Here

Transaction volumes are recovering from cyclical lows but remain near 2015 levels nationally. The capital that is deploying is heavily biased toward higher-rent submarkets. Institutional buyers are chasing quality.

Charlotte and Raleigh are telling a different story. In both markets, mid-rent and low-rent submarket transaction volumes are outperforming high-rent submarkets relative to pre-pandemic levels. That is the opposite of the national trend. Workforce housing and value-add product is trading in the Carolinas at a pace that the national data would not suggest.

For sellers of B and C assets in Charlotte and Raleigh, the buyer pool is more active than the headlines imply. For buyers, the opportunity is in the gap between national perception and local reality.

Housing as Economic Infrastructure

Secretary Flowers made a point that extends beyond real estate: housing has become a binding constraint on North Carolina’s economic growth. The state continues to attract significant corporate investment and job creation. But the ability to sustain that growth depends on whether communities can deliver housing.

In urban markets, the challenge is pace. In rural markets, the challenge is whether housing exists at all. In both cases, housing has moved from a secondary consideration to a prerequisite for economic expansion. For investors, this elevates a new set of questions: not just where demand is growing, but which markets can actually support it through infrastructure, entitlements, and political will.

Policy Is Becoming an Underwriting Input

State-level initiatives, including Opportunity Zone designations and economic development incentives, are shaping where capital flows. At the local level, entitlement timelines, infrastructure investment, and fiscal behavior are introducing new layers of complexity.

This is a structural shift. Markets that were once evaluated on demographics and job growth alone must now also be assessed through a policy lens. Investors who understand how state and local policy intersects with fundamentals will have an edge. Those who ignore it will be surprised.

What This Means

The Carolinas remain one of the strongest multifamily investment regions in the country. The demand drivers are intact. Supply is correcting. Affordability is healthy. Capital is active.

What has changed is the margin for error. A strategy built on broad market exposure is no longer sufficient. The current cycle rewards investors who can identify the right submarket, underwrite supply timing accurately, and execute through a period of transition.

The next 24 to 36 months will separate the investors who adjusted their framework from those who did not.

Connect With Greysteel’s Carolinas Multifamily Team

Navigating the evolving Carolinas multifamily market requires local expertise, policy insight, and disciplined execution.

Greysteel’s Carolinas Multifamily Team provides investors with a data-driven perspective on supply trends, rent growth, and policy impacts across Raleigh, Charlotte, and the broader North and South Carolina region.

Connect with our team today to discuss how to position your multifamily investment strategy for success in this next phase of the cycle.

More Real Estate Insights

Greysteel Advisory Expertise

Greysteel is a commercial real estate advisory firm specializing in investment sales and debt and structured finance, serving private investors, middle-market operators, and institutional clients nationwide.

The firm provides sector-focused advisory across multifamily, healthcare, and affordable housing and other commercial real estate asset classes, delivering market intelligence, capital markets expertise, and disciplined execution.